The simplest and most common company structure is a sole proprietorship. It describes a company run and owned by just one person, meaning the owner bears all responsibility.

As a sole proprietor, you have total authority over administration, operations, and decision-making. As a sole proprietorship offers simplicity and liberty in business ownership, potential entrepreneurs must understand its features.

What is a Sole Proprietorship?

A sole proprietorship is not considered legal and must not be incorporated into the company’s premises. The business and the individual trader are considered indivisible entities in a sole proprietorship. It has unlimited liability if your possessions are at risk.

According to the 2020 projection, over 75% of people in the UK are engaged in this type of business. Based on the business’s turnover, the sole proprietor must pay personal income tax. Because it requires less capital, fewer human resources, and virtually no regulatory constraints, it is the most accessible company model.

Freelance writers, consultants, small-scale service providers, independent contractors, and local retail stores are typical sole proprietorship enterprises. These companies function as sole proprietorships, which provide people total control over their operations and decision-making and enable them to be their boss. They are renowned for adjusting quickly to shifting market conditions and being agile and flexible.

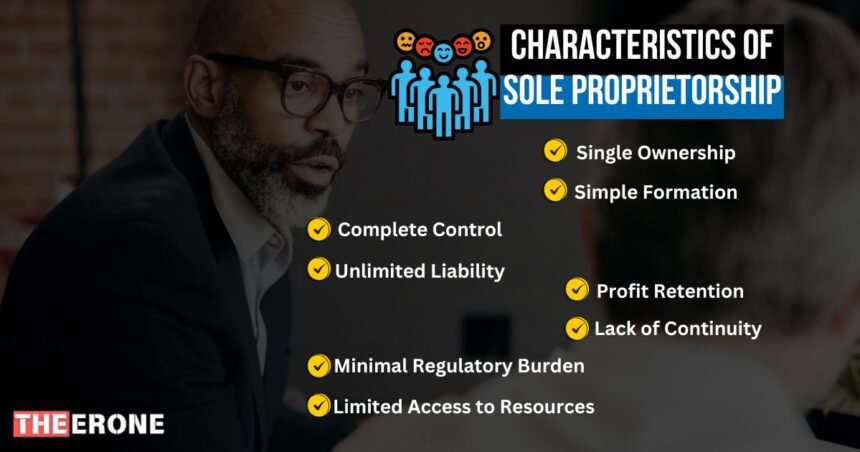

Top Characteristics of Sole Proprietorship

1. Single Ownership

A business structure known as single ownership occurs when one individual owns and controls the whole company. The individual has complete control over decision-making and oversees every facet of the business as the single proprietor. The individual is indefinitely liable; all assets and liabilities are personal property.

Examples of roles and responsibilities:

- Decision-making: The sole proprietor is responsible for making important decisions that impact the direction and performance of the business.

- Operations Management: They monitor everyday operations to ensure proper and smooth functioning.

- Financial Management: A solo proprietor’s financial duties include documenting income and expenses, paying taxes, and monitoring cash flow.

- Customer Relations: Building and maintaining customer relationships is essential to encouraging loyalty and happiness.

- Marketing and Sales: Developing strategies, promoting products or services, and driving sales growth.

- Administration: completing administrative duties, such as documentation, record-keeping, and legal compliance.

It’s crucial to remember that the owner runs a sole proprietorship and can be terminated at their request or their passing. With this company structure, people can manage their companies flexibly and freely, but they still take accountability for their accomplishments and shortcomings.

2. Simple Formation

These simple procedures will let you create a sole proprietorship:

- Choose a Business Name: Choose a name that accurately describes your company and see whether it is available.

- Register the Business: Fill out the necessary registration forms at the local government office.

- Obtain Necessary Permits and Licenses: Find out what licenses and permits your industry requires and obtain them.

- Set Up a Separate Bank Account: Open a separate bank account for business transactions.

- Keep Accurate Records: Keep thorough records of your earnings, outlays, and business operations.

- File Taxes: Complete and file tax returns for your business as the local tax authorities require.

- Comply with Local Regulations: Familiarize yourself with the local regulations and ensure compliance.

Establishing a sole proprietorship is a simple process that allows individuals to start their businesses quickly and with minimal bureaucratic hurdles. By following these steps, you can easily lay the foundation for your business and embark on your entrepreneurial journey.

3. Complete Control

You have complete authority and control over your company as a lone proprietor. You can swiftly and efficiently make decisions that enhance your day-to-day operations without speaking with partners or shareholders.

Without requiring lengthy conversations or bureaucratic processes, this independence allows you to respond swiftly to customer requests and market developments. You can adapt to changing circumstances and make successful business decisions if you move quickly and decisively.

4. Unlimited Liability

As a sole proprietor, you bear unlimited personal liability for any debts and obligations committed by your business. Your assets, including cash and real estate, may be at risk if your company encounters legal or financial problems. But there are benefits to taking full responsibility as well.

You can keep all the profits for yourself and have total control over your business’s decisions. It is crucial to carefully balance the advantages and disadvantages and consider getting the proper insurance to reduce the possible dangers.

5. Profit Retention

A sole proprietor keeps all the profits earned by the business. There are no shareholders or partners with whom to share the income. This means the owner has complete control over how to use the money. They can reinvest in the business, save it, or spend it as needed.

The owner does not have to consult anyone about financial decisions.

Sole proprietors report their business profits as personal income on tax returns, combining their business and individual earnings into one tax filing. The business owner pays taxes based on their total personal income level. Sole proprietorships are not taxed separately, like corporations or partnerships.

Advantages and Considerations

Retaining all profits gives the owner complete financial independence and simplifies managing business earnings. However, sole proprietors face personal liability for business debts or losses. Understanding tax rules ensures owners avoid unexpected financial issues. Good planning helps sole proprietors make the most of their profits.

6. Lack of Continuity

A sole proprietorship heavily depends on the owner’s presence and active involvement. If the owner becomes ill, the business operations might slow down or completely stop . In the case of the owner’s death, the business often cannot continue as before. Without the owner, no one is authorized to make critical business decisions. Customers and suppliers may lose confidence in the business during the owner’s absence. The lack of continuity can result in financial losses or permanent business closure.

7. Minimal Regulatory Burden

Sole proprietorships face fewer legal and regulatory requirements compared to other business types. The owner doesn’t need to file separate business and personal income tax returns.

Board meetings and official reports are not legally necessary. Numerous state and federal entities do not need sole proprietors to register. Most states require a simple business license or permission to operate lawfully. This simplicity makes starting and operating a business easier for individuals.

8. Limited Access to Resources

Sole proprietors often need help obtaining funds to grow their businesses. Unlike partnerships or corporations, they cannot sell shares to raise money. Most investors avoid sole proprietorships because they need guaranteed returns or shared ownership. The owner depends heavily on personal savings and small business loans for funding. Banks may hesitate to offer large loans due to the owner’s financial risk. Raising capital becomes more challenging if the business needs a solid financial history or assets.

Also Explore: What are 10 Examples of Sole Proprietors?

Advantages and Disadvantages of Sole Proprietorship

| Advantages | Disadvantages |

| 1. Full Control: Sole proprietors manage their business independently, allowing for greater control. | 1. Unlimited Liability: Owners are personally responsible for business debts and financial commitments, risking personal assets. |

| 2. Flexibility: Easy to adjust operations to meet customer needs or changing market demands. | 2. Limited Resources for Growth: Relying on personal savings and loans can restrict expansion. |

| 3. Simple Operations: No complex procedures, approvals, or formal documentation required. | 3. Difficulty in Attracting Investors: Unable to sell shares, making it harder to attract outside investors. |

| 4. Quick Decision-Making: Owners can make decisions promptly without waiting for others’ approval. | 4. Limited Ability to Expand: Growth may be slow without additional help or external funding. |

| 5. Low Start-Up Costs: Minimal upfront investment and no need for legal fees or shareholders. | 5. Personal and Business Finances are Entangled: Difficult to separate personal and business finances. |

| 6. Personalized Services: Flexibility allows owners to provide tailored services to customers. | 6. Increased Workload: Without partners, the owner bears all responsibilities, increasing workload. |

| 7. Straightforward Management: No partners or shareholders involved, making business management simpler. | 7. Risk of Personal Bankruptcy: A significant debt or lawsuit could lead to personal bankruptcy. |

Is Sole Proprietorship Right for You?

Before deciding, consider your financial goals and ability to manage risks. Sole proprietors are personally responsible for business debts and liabilities, which increases financial risks. Consider whether you have enough savings or access to funds to start the business.

This structure works best if you prefer independence and complete control over business decisions. The simple setup and low costs make sole proprietorships attractive for many small-scale entrepreneurs. Consider whether this structure can meet your future needs if you expect rapid growth.

A sole proprietorship is perfect for small businesses with a single owner and simple operations. It suits businesses with minimal start-up costs, like freelance work or online services. People who want to test a business idea often start as sole proprietors.

This structure works well for individuals who value flexibility and easy decision-making. If you wish to fully own profits, this option is an excellent choice. It is ideal for local businesses, such as shops, salons, or home-based services.

FAQs

What are the characteristics of a sole proprietorship?

A sole proprietorship has a single owner who runs the company and makes all of the decisions. It features a simple setup, easy management, and direct profit retention without shared ownership.

What are the 11 characteristics of a sole trader?

Key traits include single ownership, complete control, unlimited liability, and direct profit retention.

Other features are flexibility, easy start-up, minimal regulations, and dependence on personal resources.

What are the three characteristics that best describe a sole proprietorship?

Sole proprietorships are simple to start, easy to manage, and owned by a single person.

The owner takes all profits and full responsibility for debts and business risks.

What are the 10 disadvantages of a sole proprietorship?

Sole proprietors face unlimited liability, limited funding, workload pressure, and growth challenges.

Other drawbacks include financial risks, succession issues, low investor interest, and dependence on personal assets.

How can I decide if a sole proprietorship is suitable for me?

Before starting a sole proprietorship, consider your goals, finances, and risks.

Consider the structure’s simplicity, growth limits, and personal liability before making your choice.

Conclusion

A sole proprietorship offers business owners simplicity, complete control, and low startup costs. However, it has limited scalability, infinite liability, and difficulties luring investors. This arrangement works best for individuals or small enterprises with limited funding.

Before choosing this business structure, carefully weigh the benefits and drawbacks. Consider your long-term plans, financial risks, and ambitions as you decide. Balancing the advantages and limitations helps you choose the best path to success.